Payment processing costs: Pay by bank vs. US payment methods

Payments

March 19, 2026

|

Nick Rudy

Accepting online payments means paying a portion of your revenue in processing fees. Find out how much it costs to accept each popular payment method, plus how much you’ll save by adding pay by bank at checkout.

Pay by bank is an emerging payment method where customers connect their bank account to buy goods and services online. Instead of entering card numbers or bank details, the customer simply logs into their online banking app to add their account and make a payment.

When a customer uses pay by bank, money can move over three main bank networks (or “rails”):

Pay by bank significantly reduces processing costs, enhancing bank payments for a customer-friendly, low-risk acceptance option.

When a business accepts a payment, it is paying for the systems that authorize the transaction, move the money, settle the funds, and manage the risk around it. Here’s what is commonly included in the cost of payment processing:

When it’s all added up, U.S. businesses pay between 1.5% and 5% of every transaction in payment processing costs.

The terms “pay by bank” and "ACH" are often used interchangeably, but they rely on different infrastructure.

Traditional ACH payments rely on manual account and routing number entry, without insights into the financial account, such as available balance, account ownership, or identity verification.

Modern pay by bank solutions use API-based connections to link bank accounts and initiate payments. This technology changes the reliability and economics of accepting bank payments.

.png)

ACH transactions are typically priced as a flat fee per payment, usually between $0.20 and $1.50 per transfer, depending on transaction volume and settlement speed. These prices are very low, but there are three reasons these savings aren’t realized by businesses:

In practice, legacy ACH can carry an effective cost of around 2.0% per payment (or more) depending on factors like acceptance and return rates. Plus, there is an unaccounted loss associated with lower customer conversion and adoption.

Modern pay by bank providers typically charge around 1%–1.5% per transaction, sometimes with a small $0.15–$0.25 flat fee. At first glance, this appears more expensive than the cost of a basic ACH transfer.

However, the real cost of bank payments is driven by approval rates, conversion, and payment reliability. In order to maximize these metrics, pay by bank leverages API-based bank connections that provide real-time information like available balance, account status, and transaction history signals.

Using those signals, pay by bank transactions can use a guaranteed ACH model, where the processor assumes the return risk for approved transactions. This allows merchants to accept bank payments with greater confidence while avoiding the operational overhead of managing returns.

However, not all guaranteed ACH models perform the same. Many providers limit approvals to protect themselves from losses, which reduces the number of successful payments that actually go through.

Modern pay by bank solutions combine guaranteed ACH with real-time financial data and multiple bank payment rails. For example, transactions can be routed through guaranteed, non-guaranteed, or instant (RfP) rails depending on associated risk. This helps businesses optimize the cost and speed of every transaction.

When these systems work together, approval rates can exceed 90%, allowing businesses to scale bank payments while maintaining the cost advantages of pay by bank.

Card payments are typically the most expensive way to accept digital payments in the United States. This is because a single card transaction includes several layers of fees.

Card processing includes three main costs: Interchange paid to the issuing bank, assessment fees paid to the card network, and markup paid to the payment processor. These costs vary by card type, merchant category, and whether the payment occurs online or in person.

That total cost of card payments usually sits somewhere between 2%-5%. But many processors will just charge a flat rate for all card payments, like 2.9% + 0.30$ per transaction for most online payments.

Card costs can also extend beyond the initial transaction in the form of chargebacks. If a customer disputes a payment, the issuing bank can reverse the transaction through the card network and pull the funds back from the merchant, often with additional fees. Chargebacks typically cost merchants between $15 and $100+ per transaction in fees.

Including average chargeback losses into the average online processing fee, businesses usually pay 3.2% of every transaction in card fees.

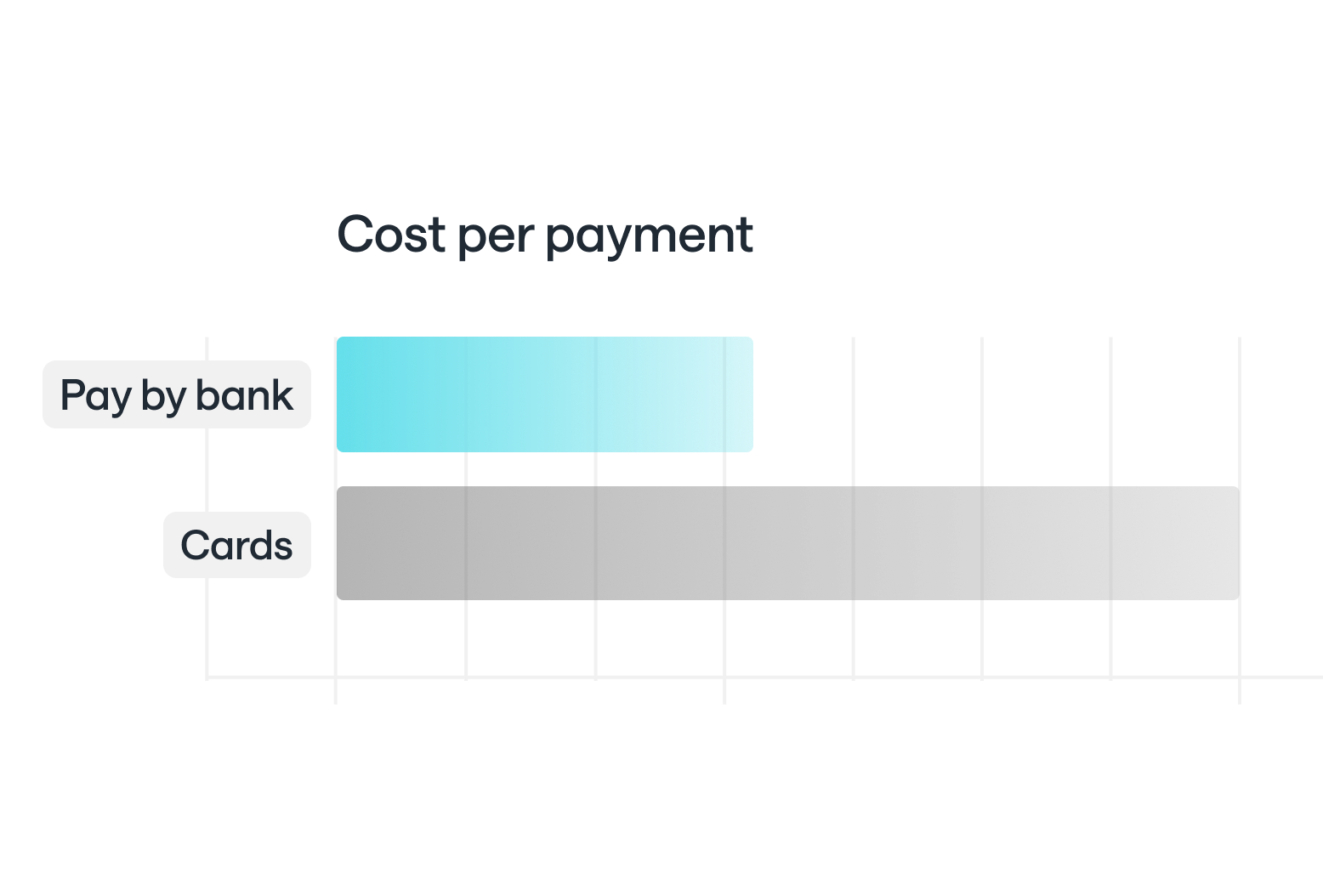

While cards are America’s most expensive payment option, pay by bank is the most affordable. This is because pay by bank is built on a system with very few intermediaries, so less middlemen take a cut of every transaction.

For recurring transactions, pay by bank adds the advantage of reducing involuntary churn caused by expired card numbers. This is a free benefit that can translate to substantial revenue gains for

On average, accepting pay by bank costs 50% less than card payments. Those savings are increased for use cases like recurring billing and high-value transactions.

Debit cards are often considered cheaper than credit cards because the Durbin Amendment caps debit interchange at about $0.21 + 0.05% for large banks. However, merchants rarely see those savings.

Most payment processors use blended pricing, meaning they charge the same rate for debit and credit cards for online transactions. As a result, businesses often pay nearly the same processing cost for debit cards as they do for credit cards.

Digital wallets such as Apple Pay, Google Pay, and PayPal allow customers to store payment credentials and complete purchases more quickly.

For merchants, most digital wallet payments are still processed using the customer’s underlying credit or debit card. As a result, merchants typically pay the same card processing fees of roughly 2% to 3.5% per transaction.

Some wallet providers also charge additional service or platform fees, which can increase the total cost even further depending on the provider.

Buy now, pay later providers allow customers to split purchases into installments while the merchant receives the payment upfront. Popular providers include Klarna, Afterpay, and Affirm.

For merchants, BNPL is one of the more expensive digital payment methods. Processing fees typically range between 3% and 6% per transaction, depending on the provider, merchant volume, and whether the plan includes longer-term financing.

These higher fees reflect the additional services BNPL providers offer. The provider assumes the credit risk, manages customer repayment, and handles fraud and underwriting. In exchange, merchants pay a premium for increased purchasing power and higher average order values.

While BNPL can increase conversion rates for certain purchases, the higher processing costs can significantly impact margins compared with traditional payment methods.

Optimizing payments can lead to considerable gains in both profit margin and revenue. By including pay by bank at checkout, your business can save 50% or more on card processing fees, while building incremental revenue growth through increases in conversion, approvals, and fraud reduction.

To help estimate exactly what the impact will be for your business, the pay by bank savings calculator allows you to input your payment volume and current processing costs to see how much you could save compared to cards or legacy ACH.

Try the calculator to see how shifting a portion of your payment volume to pay by bank can reduce processing costs and improve payment performance.